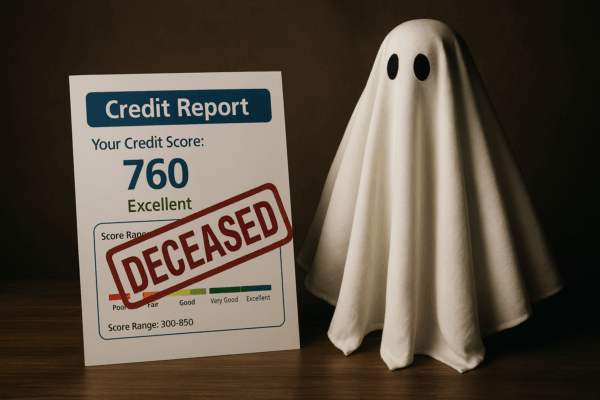

When Equifax Says You’re Dead: Your Legal Rights and How Raburn Kaufman Can Help

You’ve applied to rent an apartment. Or maybe you’re buying a car, refinancing your student loans, or switching jobs. You’ve…

You’ve applied to rent an apartment. Or maybe you’re buying a car, refinancing your student loans, or switching jobs. You’ve…

You send in a dispute with detailed documentation proving that an account on your credit report is inaccurate or fraudulent….

You’ve filled out your mortgage application, secured pre-approval, and begun planning your move. You’re expecting good news. Instead, you get…

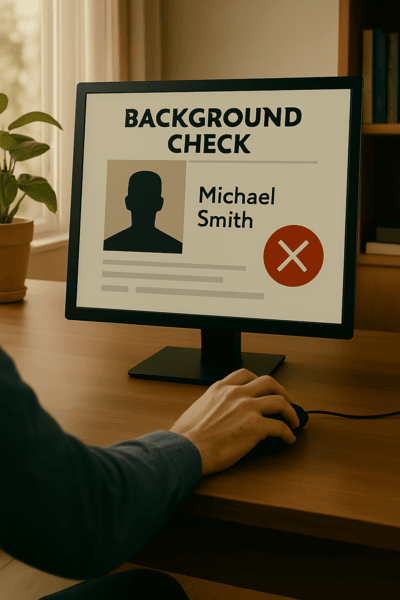

Background Check Errors Aren’t Your Fault—They’re Your Case Few experiences are as jarring as losing a job opportunity or being…

You’ve done everything right. You pay your bills on time, maintain a solid income, and have built financial stability through…

Why Having an Attorney Matters When Credit Mistakes Cost You More Than Money When people consider hiring a consumer protection…

If you have discovered a Credit One Bank card on your Equifax report that is not yours, it might be…

A DoorDash background check error can unfairly impact your chances of securing a job with the company. These errors happen…

Background checks play an important role in the hiring process for Lyft, particularly for roles that involve transporting passengers. However,…

Finding a Capital One credit card on your TransUnion credit report that you never applied for can be a sign…